The three faces of Thomas Piketty: reflections on a #1 best-seller

Chris Gregory

- Capital in the twenty-first century By Thomas Piketty

I have read Piketty’s book three times over the past month and my reaction has been different every time, due in part to the different times and places of my reading. The first time was on my kindle on a plane trip to Johannesburg and my reaction was positive. The mania driving the Piketty ‘bubble’ was nearing its peak and I, like so many others, was captured by Piketty’s persuasive rhetoric. The second time was on the return trip to Australia some two weeks later. This time my reaction was negative. Having just spent two weeks in a country with one of the most unequal income distributions in the world it occurred to me that the author of this wealthy-nation centric book had absolutely no understanding of poor-nation poverty in particular and global inequality more generally. The third time was at a more leisurely pace at my desk in Canberra. This time I was armed with a hard copy of his book, internet access to the online appendices on Piketty’s website (http://piketty.pse.ens.fr/en/capital21c2), and some of the reviews of his book. By now the ‘bubble’ had burst. Early rave reviews of his book by Nobel Prize winning economists were replaced with shock-and-awe tales of ‘fundamental errors’ in his statistical data and logical flaws in his theoretical argument. As the voices of these inequality deniers began to reach full volume I realised that it was time for me to take a more dispassionate approach. Perhaps there was something that this book had to teach anthropologists about the principles that govern the distribution of income among the top 1%, and the next 9%, in rich countries?

As noted, my initial reaction was positive because I was captured by the brilliance of Piketty’s rhetoric. Indeed, the first paragraph of the book could not have been better designed to capture the imagination of an economic anthropologist on a flight to South Africa to give a series of lectures in a Human Economy program. The book begins with an account of a massacre in August 2012 when the South African police intervened in a labour conflict at the Marikana platinum mine near Johannesburg. The miners were on strike. They had asked for a doubling of their wages from 500 euros to 1000 euros a month. The police fired on the miners. Thirty four were killed. The company then proposed a rise of 75 euros. Piketty introduces this anecdote upfront to remind the reader that the question of the distribution of income between capital and labour is a political one.

Those of us familiar with the 19th century tradition of political economy do not need reminding that politics is a brute fact of economic life; but what is this 21st century mainstream economist doing saying this? Mainstream economists are renowned for constructing ahistorical, apolitical mathematical models of the economy based on abstract assumptions that have no correspondence in reality. Piketty, a highly regarded mainstream mathematical economist, is an expert practitioner of this arcane art. So what is he doing bringing politics and history into his equations? What is he doing calling his book Capital in the 21st Century? Is Piketty the Marx of the 21st century? Why has it become a #1 best seller? Why have Nobel Prize winning economists like Stiglitz and Krugman sung its praises? Is this a radical critique of mainstream economics from within? Is the 150 year dominance of mainstream economics coming to an end?

I was hooked and spent most of the next 12 hours of my flight to South Africa totally absorbed in Piketty’s highly readable, indeed enthralling, narrative. I marvelled at his ability to write a book that is able to address everybody, be it his mathematically-inclined colleagues, statisticians, historians, sociologists, literary critics, or members of the general public. His book is also a multimedia publication that exploits the possibilities of our present digital age in a way that few others have done. The argument of the book is based on the interpretation of a massive statistical database covering some 300 years that Piketty and his collaborators in France, the UK and elsewhere have spent decades developing. The tables and figures he uses to illustrate his arguments are also available online. So too is the raw data that are used to construct the tables and charts, the sources of the data, and statistical assumptions made to massage the data into shape. Quantitative data on income distribution, Piketty rightly notes, is subject to revision and must be interpreted with extreme caution. Piketty, in classic scientific fashion, presents his raw data warts and all in the hope that quantophiles may critique it and develop a more reliable data set. Meanwhile, quantophobic readers are invited to reflect on his usage of Jane Austen and other literary classics of her time to illustrate his arguments about inherited wealth and inequality. As I was not able to access his website on my flight to South Africa so I focussed on getting to know the man and his method.

Thomas Piketty, a Frenchman trained in the mathematical economics tradition, spent his early 20s in the USA as a post-doctoral student grinding out theorems. Then, as he puts it, ‘something strange happened: I was only too well aware of the fact that I knew nothing about the world’s economic problems’ (p31). It occurred to him that the discipline of economics was ‘yet to get over its childish passion for mathematics and for purely theoretical and often highly ideological speculation, at the expense of historical research and collaboration with other social sciences’ (p 32). He dreamed of returning to the EHESS in Paris which had scholars like Claude Lévi-Strauss, Pierre Bourdieu and Maurice Godelier whom he admired more than the American Nobel Prize winning economists such as Robert Solow and Simon Kuznets. This epiphany saw him to return to Paris where he fulfilled his dream and become a director at EHESS. He now styles himself as someone concerned to rehabilitate the 19th century historical tradition of political economy. Piketty’s Capital does that by putting the question of income distribution and economic history back on the agenda. Indeed, the preface to David Ricardo’s classic work, On the Principles of Political Economy and Taxation (Ricardo 1817) could serve as the preface for Piketty’s book.

The produce of the earth—all that is derived from its surface by the united application of labour, machinery, and capital, is divided among three classes of the community; namely, the proprietor of the land, the owner of the stock or capital necessary for its cultivation, and the labourers by whose industry it is cultivated…But in different stages of society, the proportions of the whole produce of the earth which will be allotted to each of these classes, under the names of rent, profit, and wages, will be essentially different; depending mainly on the actual fertility of the soil, on the accumulation of capital and population, and on the skill, ingenuity, and instruments employed in agriculture. …To determine the laws which regulate this distribution, is the principal problem in Political Economy (Ricardo 1817: Preface).

Piketty charts the ‘different stages of society’ since Ricardo’s day in a revealing graph (see his Figure 3.2 below) that depicts what he calls the ‘metamorphoses of capital’. This shows that capital in the form of agricultural land has shrunk to virtually zero whilst capital in the form of urban housing has risen to take its place. This leads Piketty to consider just two classes, labour and capital, and two forms of income, wages and profit. The latter includes rent from land (mainly urban housing today), interest earned on financial capital and other returns from money capital of different sorts. His book analyses the changing allotment of income to these two classes over the past 300 years by considering the very factors that Ricardo highlights: the accumulation of capital, population, knowledge and technology. He finds that two ‘fundamental laws of capitalism’ regulate the unequal distribution of income we have today. The first reveals that profit’s share of national income is equal to the rate of return on capital multiplied by the capital/income ratio. The second states that the capital/income ratio is equal to the savings rate divided by the growth rate in national income. His principal finding is that forces of income divergence have outweighed the forces of convergence since the 1970s as the rate of return on capital (r) has exceeded the growth rate (g). In other words, r > g means that the rich are getting richer and the poor are getting poorer. This thesis has a Marxist ring to it but Piketty argues that Marx’s apocalyptic vision of capitalism was wrong: the rate of profit has not tended to fall as Marx predicted because the long term trends in the statistical data reveal that r > g > 0.

What policy implications follow from these empirical findings? Picketty informs us that he belongs to a generation that turned eighteen in 1989 when the Berlin Wall fell. News of the collapse of communist dictatorship aroused in him not the slightest nostalgia for the regimes of the Soviet Union. To the contrary, he was ‘vaccinated for life against the lazy rhetoric of anticapitalism’ (p30). Even though inequality is his main theme, he has ‘no interest in denouncing inequality or capitalism per se’ (p30). As a political economist he is a statesman in the Ricardian tradition rather than a revolutionary in the Marxist tradition. His primary concern is with taxation policy and the final section of his book explores the implications of his findings for the development of an optimal tax. The title of the book is, therefore, somewhat misleading. He problematic is neo-Ricardian rather than neo-Marxian. Had he imitated Ricardo rather than Marx the book would have been called On the Principles of Political Economy and Taxation in the Twenty-First Century. But an esoteric Ricardian title of this kind would not have made for a best seller; Marx’s name is much better for business these days. Picketty’s book, then, should not be judged by its cover. The title does not signal a rebirth of Marxian ideas but their re-death; Capital in the Twenty-First Century is the name tag on yet another coffin containing Marx’s stinking corpse.

***

The second time I read Piketty’s book was on the 12 hour flight back to Australia two weeks later. This time my reaction was negative. The brilliance of his rhetoric, it occurred to me, is a sham. Picketty is Janus-faced and his decision to hide his Ricardian problematic behind a Marxian facade is the outward expression of this. The book is full of examples of his two-facedness. Take his method for example. While his problem is expressed in the historical and political tradition of 19th century Ricardian political economy, his answer was in the narrowest apolitical, mathematical tradition of 20th century mainstream economics. My two weeks in South Africa—the first time I had been there—literally knocked some sense into me about the reality of global inequality today. One does not need statistics of the kind that Piketty produces to know that South Africa is one of the most unequal countries in the world today. The mansions of the wealthy in the cities are hidden behind high electrified fences often topped with extra rolls of razor wire; the shacks of the poor are hidden from view in the outer suburbs. The ‘laws’ of political economy that Piketty uncovers may help us understand the relative shares of income that go to the workers and the owners of a platinum mine but they do not even begin to grasp the reality of the political relations that link the superaltern rich in South Africa to the unwaged subaltern poor. I began to realise this as I wandered around the streets of Pretoria and Durban, as I listened to my hosts in the Human Economy program (Keith Hart and John Sharp), and as I read and discussed the papers produced by their interdisciplinary team of doctoral and post-doctoral scholars. I learned about the everyday corruption of traffic cops in Zimbabwe, the unfair competition faced by indigenous Lesotho businessmen under colonial rule, the devastation the rivalry between the USA and the USSR brought to the people of Angola, and many other aspects of life for the poor in southern Africa. As I began to reflect on this in the light of my own fieldwork experiences in India, PNG and Fiji it occurred to me that Picketty has absolutely no understanding of the principles shaping the distribution of income in relatively poor countries. This much he admits because the statistical data are not available; but when I came to think about Enron, Lehman Brothers and the subprime crisis in the USA I began to wonder how much he understands about inequality in the wealthy countries. Neither Enron, nor Lehman Brothers nor subprime lending rate a mention in the index of his book. And what does he say about the Bush bailout that ensured that Wall Street was able to socialise its losses and privatise its profits? Nothing.

Further digging into his text reveals that the respect Picketty pays anthropologists such as Lévi-Strauss, Bourdieu and Godelier is a mere gesture. He does not refer to them in his bibliography and obviously has no understanding of economic anthropology and of how the tribes and peasants of yesteryear were articulated with the dominant capitalist mode of production. Polanyi was the first economic historian to take this problem seriously in his 1944 classic The Great Transformation: The Political and Economic Origins of our Time. The old trichotomy of tribes, peasant and capitalist—conceptualised as reciprocity, redistribution and money-making by Polanyi—has morphed into an opposition between the plutocracy and the precariat today. Piketty makes no attempt to come to terms with Polanyi or the attempts that have been made to bring him up to date. How can any self-respecting economic historian in the Political Economy tradition write about the economic history of global capitalism over the past 200 years without mentioning Polanyi? This is a bit like a physicist writing about relativity theory without mentioning Einstein.

Polanyi is not the only major economic historian he ignores. He refers to the period from 1870 to 1914 as the ‘belle epoque’ but makes no reference to the fierce debates that raged between conservatives such as Hobson and Marxists like Lenin over the nature of the inter-imperialist rivalries that shaped the politics of that era. He rightly notes that the period 1970 to 2014 bears some disturbing similarities to 1870-1914 but does not consider the fact that the study of inter-imperialist rivalries between USA and China may help us understand the economic history of this contemporary period.

The fact of the matter is that Piketty is not an economic historian and nor is he a theoretical revolutionary; he is a mainstream economist in the classic marginalist tradition of mathematical economics (but with some minor reservations: see p 333). Picketty naively believes that the economic history of capitalism over the past 300 years can be reduced to two insanely simple mathematical ‘laws’.

His first so-called ‘fundamental law’ is nothing more than an algebraic manipulation of a simple accounting identity. In a nation where the only people who earn income are workers and capitalists the annual national income (I) is the sum of wages (W) paid to workers and the profit (P) received by the owners of capital. This can be written in equation identity form as,

I ≡ W + P.

If the national income in a given country for a given year was 1000 million euros, and the wages bill was 700 million euros, then it follows that profit, the income going to the owners of capital, will be 300 million euros. The percentage share of national income going to labour and capital is calculated by dividing each side of the equation by I. Thus:

I/I = W/I + P/I

= 700/1000 +300/100

= 0.70 + 0.30

= 1

Or, to use percentages, wage’s share is 70% of national income and profit’s share is 30%.

As every investor knows, if 6,000 million euros is invested in a bank for one year at an interest rate (r) of 5% then the profit (P) on capital (C) will be 300 million euros. In other words, profit income is equal to the interest rate times capital. This has the mathematical form.

P = r x C

= 0.05 x 6000

= 300

His first ‘fundamental law’ is derived by noting that the profit share is P/I and that P equals r x C. Thus substituting the latter into the former gives:

P/I = r x C/I

In other words, the share of income going to profits depends on the rate of profit times the capital/income ratio. If we use the numbers of the example above we find that this law gets us back to the accounting identity from which we started.

P/I = r x C/I

= 0.05 x 6000/1000

= 0.05 x 6

= 0.30

Given that the share of national income going to the owners of capital is equal to the rate of return times the capital/income ratio, it follows, ceteris paribus, that the profit share goes up when the interest rate rise or the capital/income ratio rises. The Latin phrase is oft resorted to by mainstream mathematical economists because if other things are not equal then we can’t be sure what will happen. For example, if the interest rate rises and the capital/income ratio falls then we cannot say what will happen to profit share unless we know the quantitative extent of the changes. Piketty’s second ‘fundamental law’ is designed to deal with the situation when the ceteris paribus assumption does not hold. Whereas the first ‘law’ is accounting identity based on a snapshot at a given point in time, the second law is a ‘dynamic’ one based on long-term statistical trends. This ‘law’ holds that, in the long run, the capital/income ratio is determined by the ratio of savings rate (s) to the growth rate (g). In equation form:

C/I = s/g

This ‘law’ takes us from the identities of the double-entry bookkeeper to the fantastic assumptions of the mainstream economist. As Piketty notes, the law is valid ‘only if certain crucial assumptions are satisfied’ (p168). He sums up these crucial assumptions in the following way:

[T]he law … s/g does not explain the short-term shocks to which the capital/income ratio is subject, any more than it explains the existence of world wars or the crisis of 1929—events that can be taken as examples of extreme shocks—but it does allow us to understand the potential equilibrium level toward which the capital/income ratio tends in the long run, which the effects of shocks and crises have dissipated (Piketty 2014: 170).

As Keynes famously remarked, ‘In the long run we are all dead. Economists set themselves too easy, too useless a task if in tempestuous seasons they can only tell us that when the storm is past the ocean is flat again’ (1924: 80, emphasis in original). Piketty’s analysis, then, assumes that the sea is always dead calm. For the bottom 50% in the income pecking order, by contrast, the tempest is an everyday phenomenon. Even when the sea is calm they are in danger. As Tawney famously noted in his study of Land and Labour in China, there ‘are districts in which the position of the rural population is that of a man standing permanently up to the neck in water, so that even a ripple is sufficient to drown him’ (Tawney 1966: 77), an idea that has been developed by James Scott (1976) in his classic text on the Moral Economy of the Peasant.

The reader will recall that Piketty begins his book with an anecdote about the Marikana platinum mine and that the purpose of this was to remind us that income distribution is a political problem. However, by the time Piketty gets to his second law he has forgotten his own lesson: relatively minor political events like this, along with ‘extreme shocks’ like world wars, are ‘dissipated’ in the long run when his deterministic mathematical law of economics asserts itself. In sum, politics is secondary in Piketty’s Janus-faced analysis; political upheavals are mere short-term ‘shocks’ in the long-run journey to an economic equilibrium determined by Piketty’s ‘fundamental laws’ of capitalism.

I come now to Piketty’s proposed solution to the problem of growing income inequality: his policy of a global tax on capital. This is, as he admits, utopian (p 515). It requires the nations of the world agreeing on a tax schedule and on how to distribute the revenues collected. Nevertheless, he believes that such a utopian ideal is ‘useful’ and has developed a mathematical formulation of his argument which he published in Econometrica (Piketty 2013). But wait, why do we need a mathematical proof of the usefulness of an idea that bears no correspondence in reality? Is this not an example of a ‘childish passion for mathematics’ from someone who has accused his mainstream colleagues of having this self-same childish passion? Janus-faced Piketty says one thing to his general audience, quite another to the brotherhood of mainstream mathematical economists. He seems concerned to maintain his social status as a member of the latter while appearing to be a critic of it in the eyes of the former.

How to explain Piketty’s two faces? One possible answer is the cultural specificities of French political life. While talk of income inequality is radical in modern America, it is a political given in France. A leftish gloss is essential if you are to be taken seriously in Paris; but by these French standards his book was still not left-wing enough. The French version of Capital never became a #1 best-seller in France and was only in 192nd place in April 2014. As a left-wing French reviewer correctly noted, there is no discussion of ‘social and cultural domination, violence, relegation, exploitation, alienation at work, class, struggle etc’ (http://www.economist.com/blogs/charlemagne/2014/04/thomas-piketty). In other words, Piketty has no understanding of the reality of politics.

Piketty served as an economic advisor to François Hollande, France’s Socialist president, during his 2012 election campaign and was closely linked with Hollande’ proposal to introduce a millionaire tax of 75% on top incomes. Piketty believed that this tax was going to be a world trend setter but it was denounced by other advisors to Hollande and ruled unconstitutional by a French court. This story serves to remind us that tax policy, too, is a political problem not a mathematical one.

***

My third reading of his book was made in my study after my return from South Africa. This time I had access to the 685 page hard copy version of his book, to Piketty’s web site, and to the many reviews of the book that had been published and were available online. The excitement I experienced on my first reading and the irritation I felt on the second reading had passed. I was now in a position to undertake a more dispassionate view of the publishing sensation that is Piketty’s book. What has this book to offer anthropologists interested in political economy, economic history and economic anthropology? Quite a lot if one is fully aware of the limitations of its scope and method. Piketty cannot hold a candle to Ricardo as a political economist, nor to Polanyi as an economic historian and nor to Godelier as an economic anthropologist. But he is a good double-entry bookkeeper when it comes to the national accounts of wealthy nations. The data Piketty and his bookkeeping friends have assembled are worthy of close analysis because they enable us to pose some interesting questions about kinship and the economy among the super-rich and what he calls the patrimonial middle class.

Piketty’s conception of ‘capital’ is the simple one used by the double-entry bookkeeper, not that used by Marx. This is not to belittle the bookkeeper’s concept. To the contrary, without the meticulous labour of the double-entry bookkeeper we would know nothing about capitalism. The bookkeeper’s forte is the humble transaction. He meticulously records who gave what to whom, when, where and why. If the parent/child relation is the atom of kinship then the buyer/seller relation in a transaction is the atom of commerce; just as we cannot understand the history of the family without the labours of the genealogist, so we cannot understand capitalism without the labours of the double-entry bookkeeper and the national income accountant. The national income of a country is the aggregation of countless transactions. The business accountant sorts his transactions into ledgers and, at the end of the year, prepares his profit and loss account and balance sheet. The balance sheets give a snapshot at a point in time, the profit and loss account the income flows between two points in time. Piketty’s two ‘laws’ are the national-level analogue of these two generic methods of analysing a year’s worth of daily transactions.

The accountant’s job is not a simple one because he has to contend with difficult valuation problems that have no simple answers. For example, what prices does he use to value the capital stock? Should they be based on historical cost price or current replacement cost? These problems ensure that bookkeeping is always a creative art and that the accountant’s figures are always ‘rubbery’ even though he may be the most virtuous soul in the world. Capital in the physical form of, say, an industrial steel plant could not be colder or harder; but the money value of this capital in the accountant’s books could not be warmer or fuzzier. The accountant has to reduce a diverse range of machines and other physical equipment to a single number of a monetary kind. Many of the reductive calculations he makes are legitimate, some are of the ‘grey area’ kind, and some may be illegal (as the Enron case illustrates). The national income accountant, for his part, constructs his conceptions of the capital/income ratio from the rubbery data the business accountant produces. Piketty, as a national income accountant, has worked very hard (with his colleagues) to construct new time series data which, he rightly notes, ‘are more extensive than any previous author has assembled, but they remain imperfect and incomplete’ (p571, emphasis added). He too has had to ‘massage’ his data but, in the interests of scientific transparency, provides online details of how he has done this.

Piketty’s answers to the question of income inequality he poses may reflect his inability to exorcise his passion for mathematical models of the economy, but the conceptual framework that informs his approach to organizing his original statistical data is very useful because it allows the reader to pose their own questions and to develop different answers.

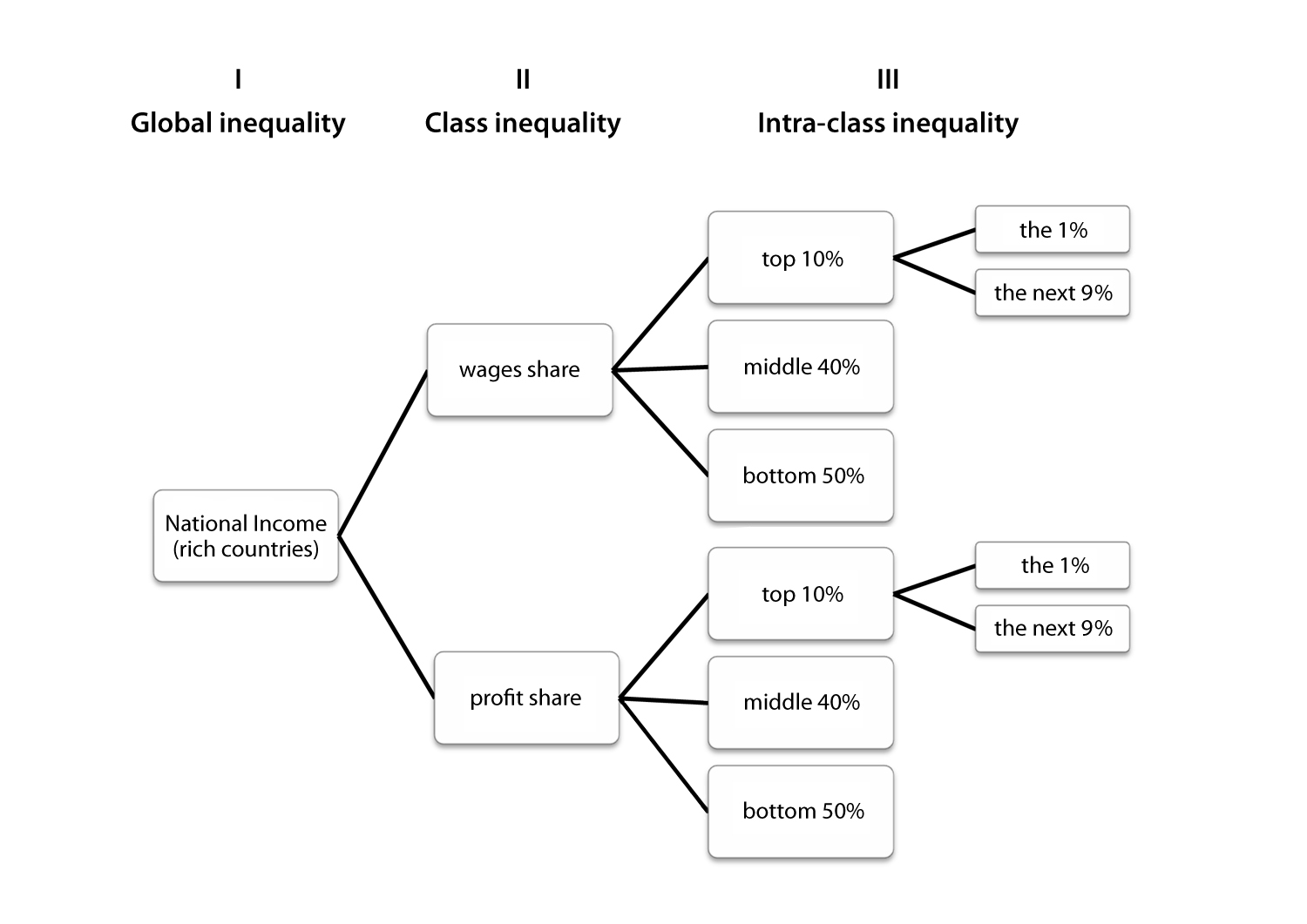

Capital in the 21st century has a logically-coherent four-part structure. The first three parts are descriptive and pose the problem of inequality, the fourth is prescriptive and proposes a tax to overcome the problem. The first three parts deal with income inequality defined firstly as global inequality between nations, secondly as class inequality between capital and labour, and thirdly as intra-class inequality within capital and labour considered separately. Wages, the income from labour, is divided into three sub-categories: the top 10%, the middle 40% and the bottom 50%. Profit, the income from capital, is similarly sub-divided. The top 10% of both classes is further sub-divided into the top 1% and the next 9%. In the following diagram I depict the conceptual framework Piketty employs.

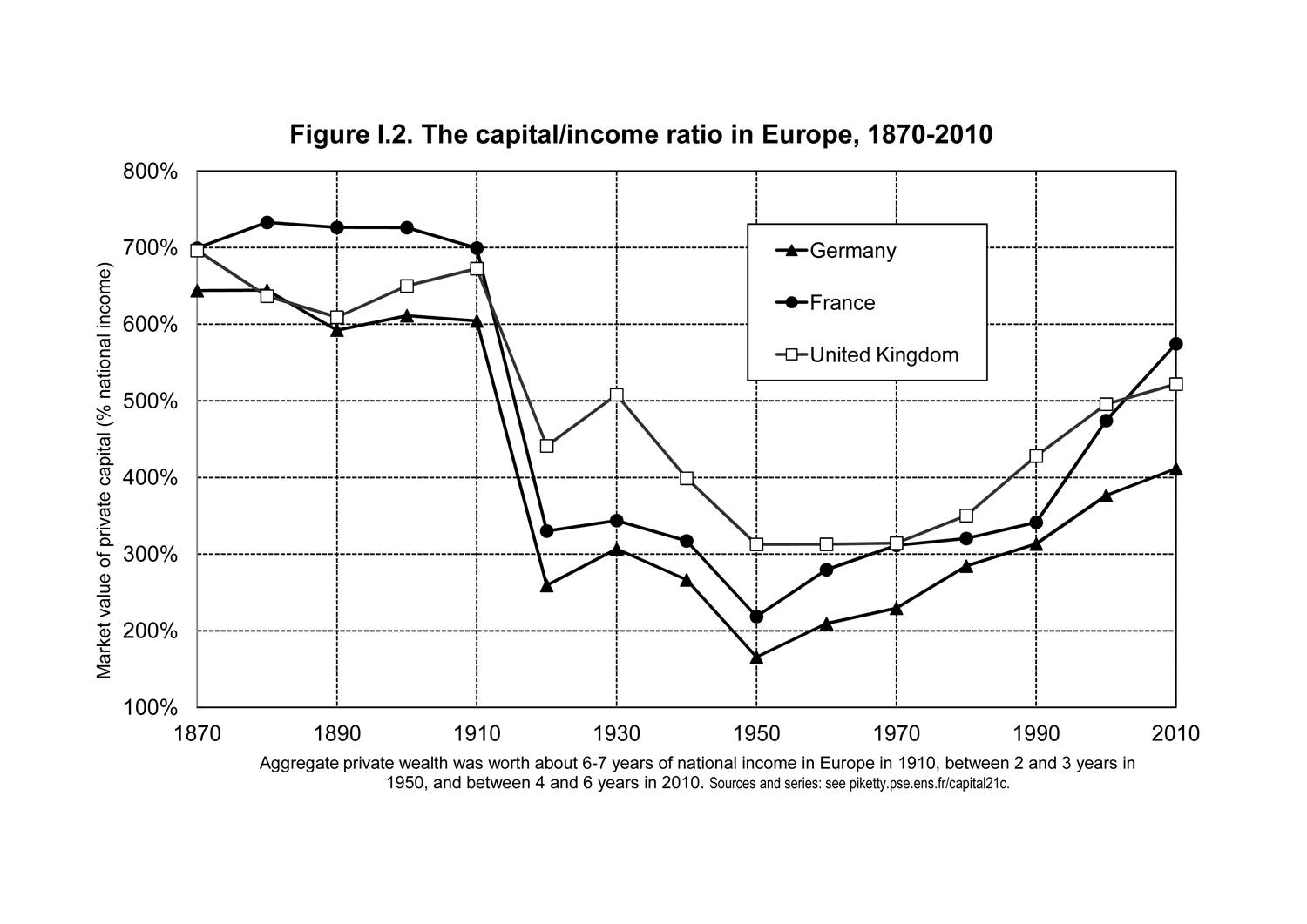

The general flavour of his three-tiered empirical findings on income inequality can be gleaned from examining some of his own charts. Piketty’s Figure 1.2 shows the capital/income ratio for France, Germany and UK for the period 1870 to 2010. It reveals the obvious fact that world wars are destructive and that the period since 1970 has been very good for capital. These countries have not yet returned to the ‘belle époque’ of the late 1800s but they are fast getting there.

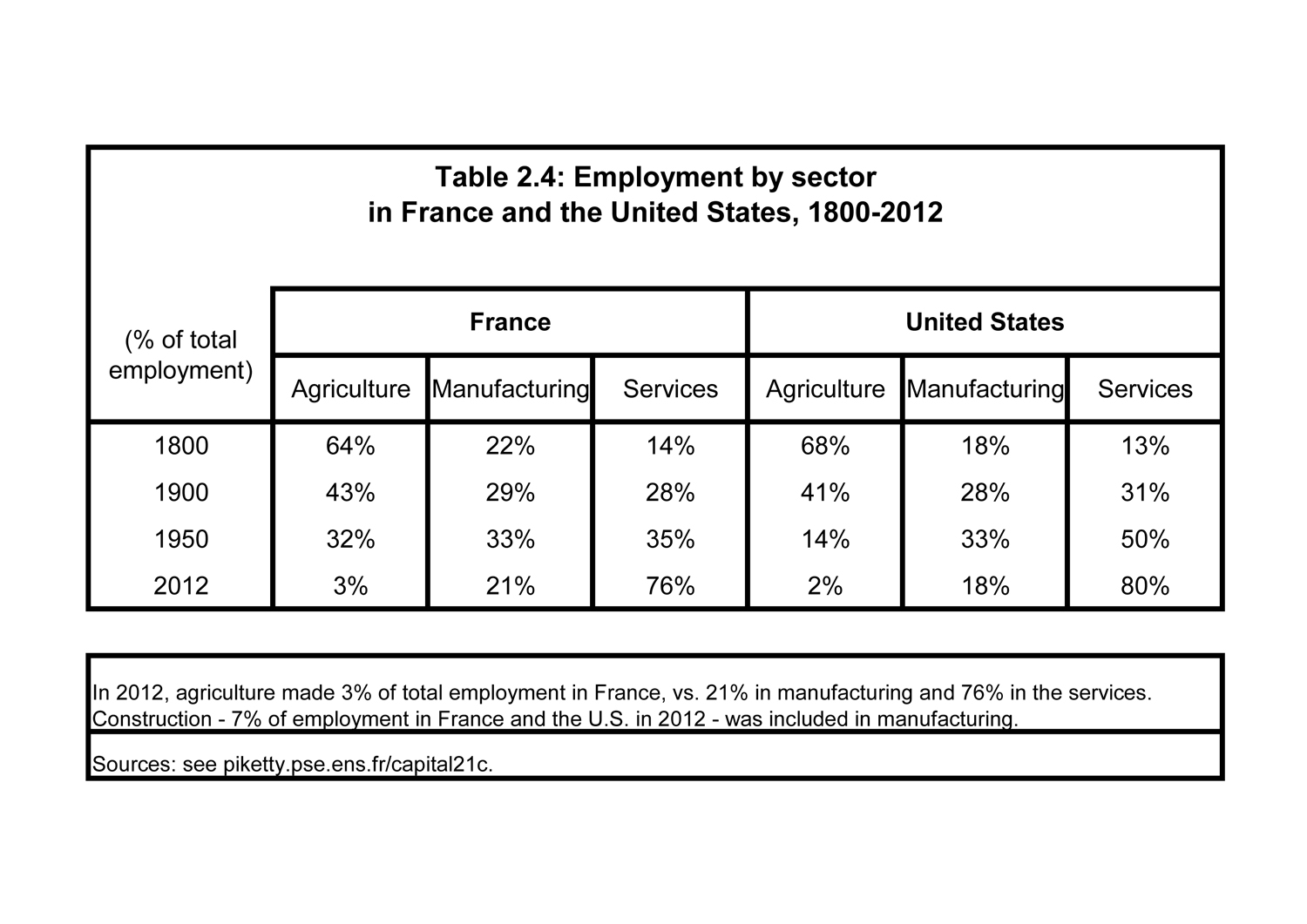

This quantitative change in the capital/income ratio has been associated with a qualitative change in the structure of capital in wealthy countries over the past 200 years. There has been a complete inversion in the relative importance of different types of capital: primary industries dominated in the early 1800s and tertiary service industries in the early 2000s; secondary industries, for their part, have maintained their middle ranking, increasing in importance until the 1950s and falling after that as the process of de-industrialisation (and Asian industrialisation) began. Piketty’s Table 2.4 shows how both France and the United States went through this metamorphosis in much the same way.

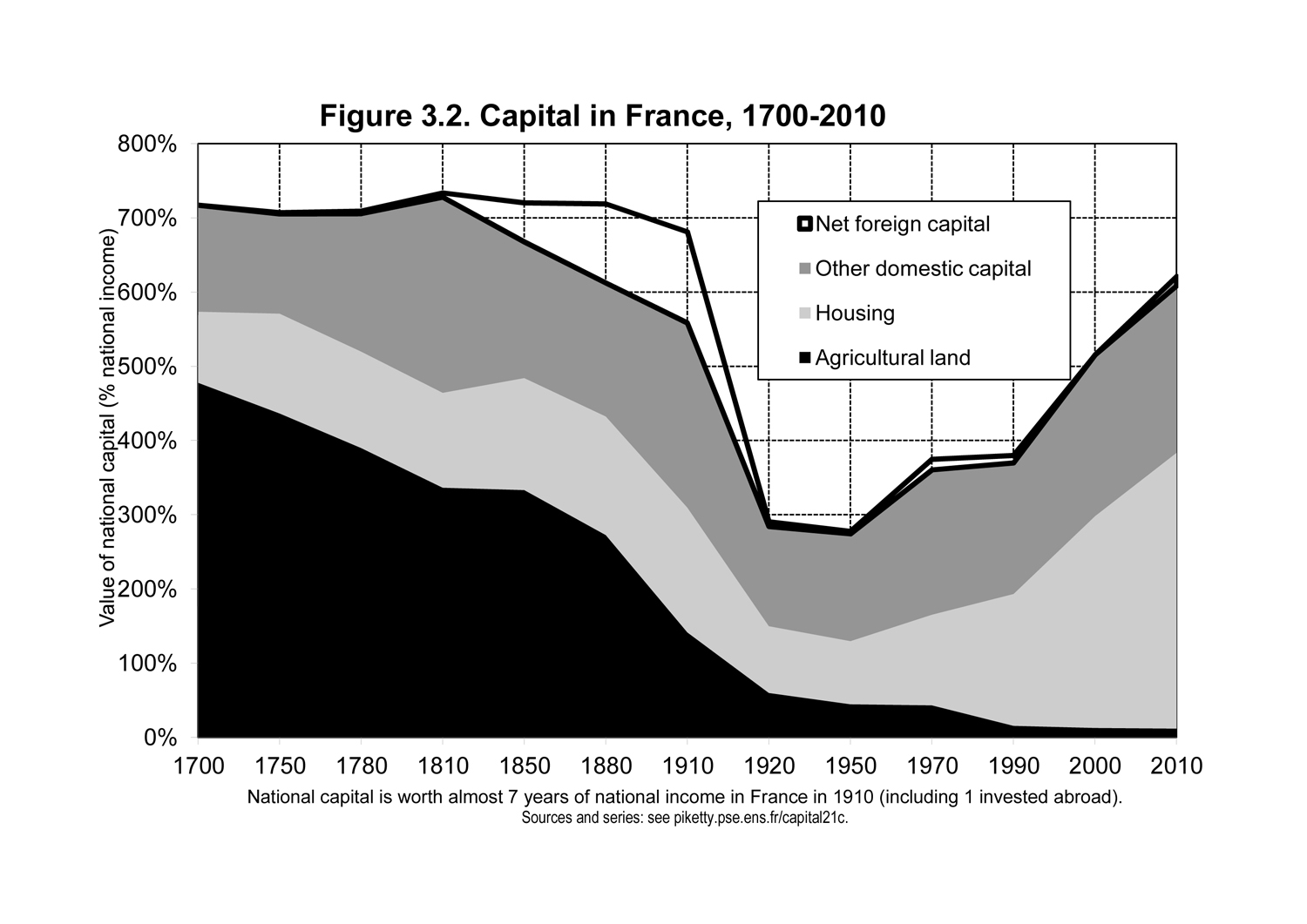

The rise of the service sector in the wealthy nations has changed the qualitative composition of money capital. Piketty’s Figure 3.2 shows the make-up of French capital over the 300 years from 1700 to 2010. The absolute size of capital has just about returned to its pre-WW1 levels but with agrarian capital falling to almost zero and urban housing capital rising in inverse proportion. His data tell a similar story for other wealthy countries.

This process was also associated with demographic transition: population growth rates in Europe were among the highest in the world in the period 1700-1820; they are now among the lowest; those for Africa and Asia, by comparison, have boomed (see Piketty’s Table 2.3).

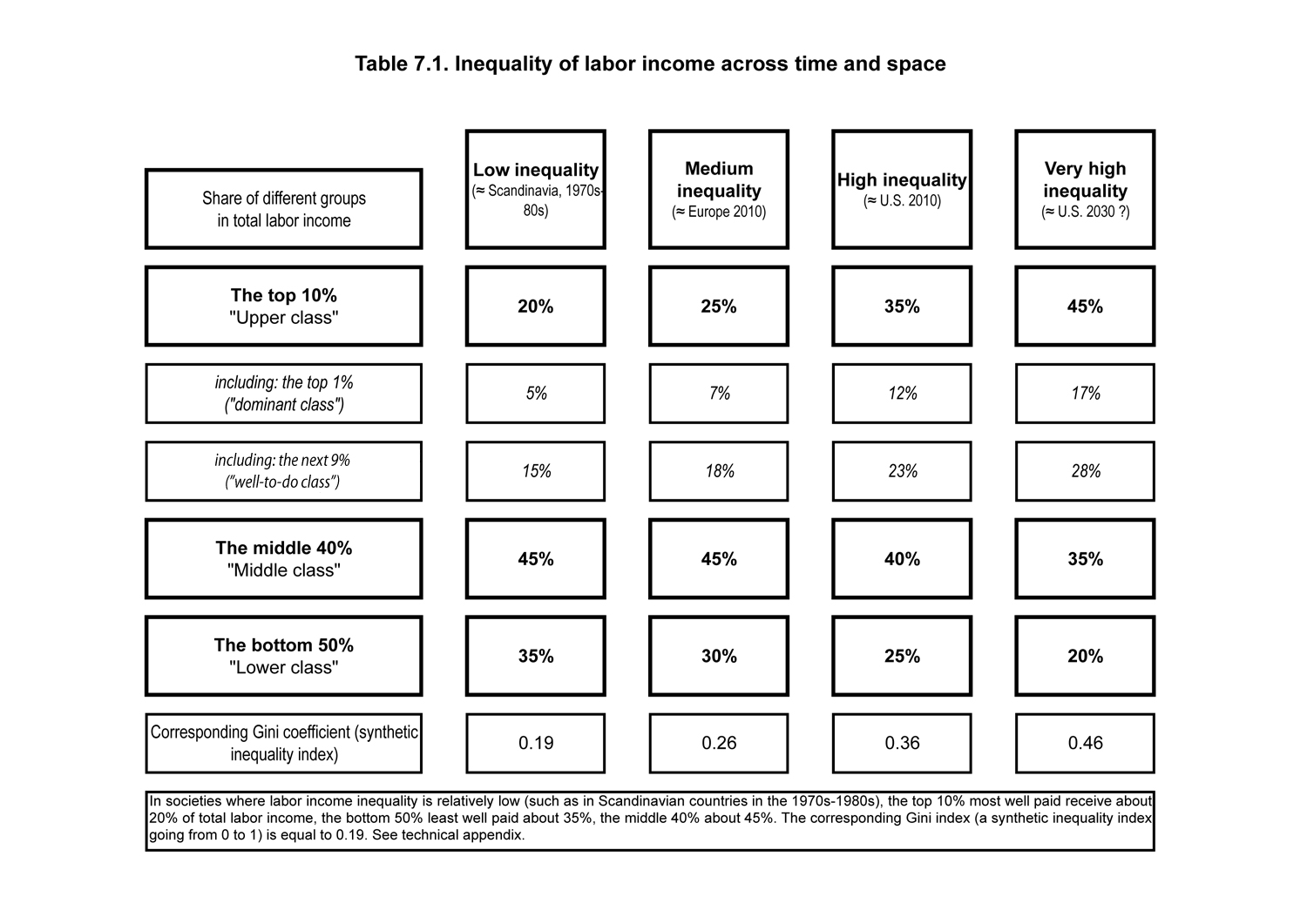

Whereas Marx’s analysis of capital focussed on class inequality—the relative shares of income going to capital and labour—Piketty moves the debate along by examining intra-class income inequality. It is here that the novelty of Piketty’s findings comes to the fore. His Table 7.1 shows the inequality in labour income across time and space. The top 10% of workers in the USA earn 35% of labour income whilst the top 1% earns 17%. This is due largely to the rise of a super managerial class who set their own salaries and pay themselves annual bonuses amounting to millions of US dollars. The USA beats Europe on this score and Piketty predicts that this source of inequality in the USA will worsen over the next two decades.

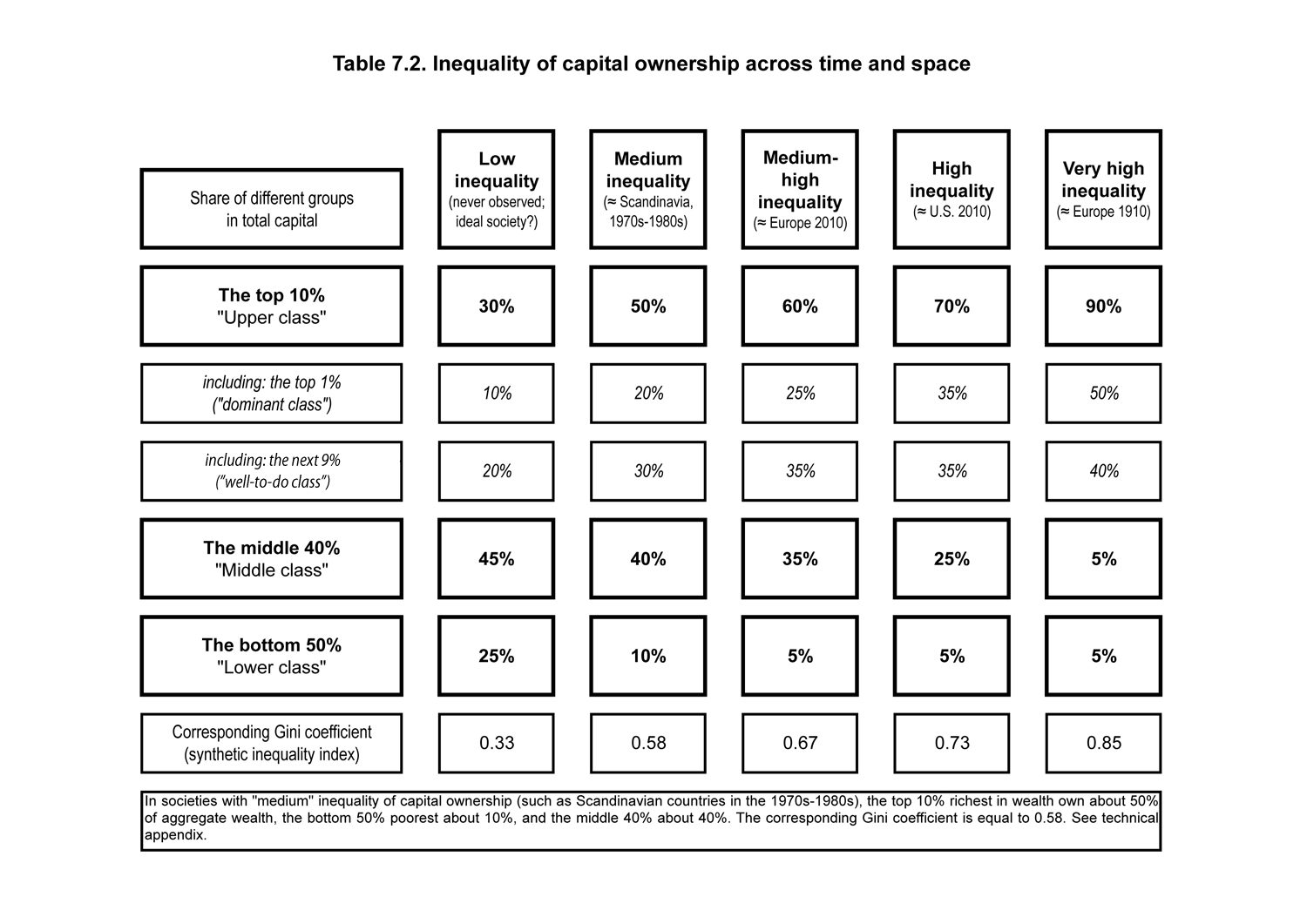

When it comes to inequality in income returns from capital, Europe beats the USA. As his Table 7.2 shows, the top 10% of capital owners in Europe take home 90% of all profits, whilst in the USA they take home 70%. When the data on these two charts are considered together, and we look at the mixed income of the top 10%, then we find what Picketty calls the ‘two worlds’: the top 1% in which income from capital predominates; and the next 9% in which income from labour predominates (p280). This statistical fact raises the much debated issue of how to define a social class and raises the question of the adequacy of his conceptual analysis. How should the salary of a CEO who controls capital be classified? Is it an intra-class division of labour income inequality or does it occupy a more ambiguous space?

The familial implications of all these statistics become apparent when we examine data on the rate of growth of output. Rates of growth in output, Piketty notes, can be conceived of in generational terms. If we assume this to be a 30 year period then a growth rate of 1% per year means a cumulative growth rate of 35% over 30 years. This, he notes, implies major changes in lifestyle and employment from one generation to the next.

Over the period 1700-2010 Europe grew at an average rate of 1% compared to 0.5% for Africa and 0.7% for Asia. During the period 1913-1950 Europe grew at 0.9% per year compared to 0.2% for Asia. Both grew at over 3% for the period 1950-1970 but Asia kept growing at this rate after that while Europe fell to 1.9% (See his Table 2.5). These rapid changes have made inherited wealth less decisive as large fortunes where accumulated by the newly super rich. But as growth rates fall back towards 1% inheritance once again becomes important. Piketty argues that this has been particularly important for the ‘patrimonial’ middle classes who constitute the ‘next 40% percent’ category. We are back to the world of Jane Austen where inheritance was crucial for the reproduction of wealth, although marriage arrangements have obviously changed since then.

Here is a challenge for the anthropologist. George Marcus (1983) pioneered the study of the transmission of wealth among the super elite but has since moved on to other topics. Doubtless other scholars are studying familial transfers of money among the super elite and the patrimonial middle classes but it does seem to me to have been a neglected area. Ethnographers working on the wealthy today have tended to locate themselves in Wall Street and other trading financial centres rather than in the domestic moral economies of the families from whence the financial traders and owners of wealth come.

Piketty, I decided after my third reading of his book, has three faces not two: he is, firstly, a political economist in his approach to the question of income distribution in wealthy countries; he is, secondly, a mainstream economist in his approach to the answers he gives to the question he poses; and he is, thirdly, a national income accountant when it comes to statistical data collection on the distribution of income. His originality and importance lies in his role as the latter. We all need data of the kind he has produced no matter what our theoretical perspective might be. As he rightly notes, the statistical data he produces must be complemented with data collected using different methods and interpreted using a variety of inter-disciplinary approaches. We must never forget, as he reminds us at the beginning of his book, that income distribution is first and foremost a political problem. This big rambling book has the capacity to excite readers, to irritate them, and to inspire them to think about the very important problem of income distribution he confronts. This, at least, is how it has affected me. It is worth reading three times. It is a wonderful smorgasbord of dishes, some sweet, others sour; it has something for everyone but one needs to choose carefully; one must avoid being influenced by the inflated rhetoric of the windbags who have over-blown the Piketty bubble or the deniers who are now trying to burst it.

BIBLIOGRAPHY

Keynes, J.M. 1924. A Tract on Monetary Reform. London: Macmillan.

Marcus, G. E . 1983. Elites: Ethnographic Issues. Albuquerque: University of New Mexico Press.

Piketty, T. 2013. “A Theory of Optimal Inheritance Taxation.” Econometrica no. 81 (5):1851-1886.

Ricardo, David. 1817. On the Principles of Political Economy and Taxation. Edited by Piero Sraffa and Maurice Dobb. Vol. 1, The Works and Correspondence of David Ricardo. Cambridge: Cambridge University Press, 1975.

Scott, J.C. 1976. The Moral Economy of the Peasant: Rebellion and Subsistence in Southeast Asia. New Haven: Yale University Press.

Tawney, R.H. 1966. Land and Labour in China. Boston: Beacon Press.

Please join our mailing list to receive notification of new issues